May 16 – Read the newsletter below for the latest Mortgage Banking and Consumer Finance industry news, written by Ballard Spahr attorneys. In this issue, we discuss Colorado’s rate exportation litigation, PA Department of Banking and Securities updated interpretation of the word “money,” CFPB’s Office of Minority and Women Inclusion’s annual report, and much more.

- This Week’s Podcast Episode: The U.S. Supreme Court’s Pending Ruling on National Bank Preemption: A Discussion of Cantero v. Bank of America, N.A.

- SEPA SHRM and Ballard Spahr LLP 2024 HR Legal Summit

- HUD, Fannie Mae, and Freddie Mac Issue Reconsideration of Value Guidance to Combat Appraisal Bias

- CFPB Issues New Report on Price Complexity and Highlights Implications for Junk Fees Initiative

- Final Guidance on Workplace Harassment Published by EEOC

- Director Chopra Issues Statement on FDIC/OCC/FHA Proposal on Incentive-Based Compensation Arrangements

- CFPB and European Commission Report on Coordinated Efforts Concerning Consumer Financial Protection and Identify Emerging Technologies as an Area of Shared Interest

- Ninth Circuit: Arbitration Clause Prevails in “True Lender” Challenge Against OppFi

- Colorado Rate Exportation Litigation: Why Colorado and the FDIC are Wrong About Where a Loan is Made for Purposes of DIDMCA Section 525

- Plaintiffs File Reply in Support of Motion for Preliminary Injunction in Colorado Rate Exportation Litigation

- Colorado Passes AI Regulation

- PA Department of Banking and Securities: Virtual Currency Is “Money”

- CFPB’s Office of Minority and Women Inclusion Publishes Annual Report to Congress

- Looking Ahead

On February 27, 2024, the U.S. Supreme Court heard oral argument in Cantero v. Bank of America, N.A., a case involving the effect of the Dodd-Frank Act on the scope of preemption under the National Bank Act (NBA). The specific question before the Court is whether, post-Dodd-Frank, the NBA preempts a New York statute requiring banks to pay interest on mortgage escrow accounts. The decision, however, could have ramifications well beyond the specific New York law at issue. This episode repurposes a recent webinar roundtable and brings together as our guests four attorneys who filed amicus briefs with the Supreme Court: Jonathan Y. Ellis, William M. Jay, and Matthew A. Schwartz, partners in private law firms, and Professor Arthur E. Wilmarth, Jr. After we review the procedural history of Cantero, our guests discuss the arguments made in favor of and against preemption in their amicus briefs and share their reactions to the oral argument and predictions for how the Court will rule.

Alan Kaplinsky, Senior Counsel and former Practice Group Leader in the firm’s Consumer Financial Services Group, moderates the discussion.

To listen to the episode, click here.

SEPA SHRM and Ballard Spahr LLP 2024 HR Legal Summit

Legal updates have become more important than ever in the evolving workplace in a post-pandemic era. Stay on top of the latest trends and advice on how to handle the new evolving workplace by participating in SEPA SHRM’s premiere legal conference!

The Southeastern Pennsylvania Chapter (SEPA) of SHRM is excited to host our 12th Annual HR Legal Summit, where over 200+ HR Professionals gain practical information on Labor and Employment Law compliance for 2024 and beyond. There will be a panel of Ballard Spahr speakers on a variety of topics geared to HR and decision makers on how to stay abreast of various legal changes to keep their organizations compliant. Additionally, there will be opportunities for engagement in question and answer sessions and sponsors/exhibitors to provide goods and services that would be of interest to HR professionals.

Thursday, September 19, 2024

Presidential Caterers

2910 Dekalb Pike

East Norriton, Pennsylvania 19401

Program: 8:00 AM – 4:30 PM ET

7:15 AM ET | Doors Open

8:00 AM – 4:30 PM ET | Program

Early Bird Registration Deadline now through August 18, 2024.

Click here to learn more about becoming a Sponsor or Exhibitor

Ability to earn SHRM and HRCI recertification credits.

For more information about the conference, sponsorship opportunities, or exhibiting, please contact Laurie Sample at sepa-administrator@sepashrm.org or visit the 2024 2024 HR Legal Summit event.

HUD, Fannie Mae, and Freddie Mac Issue Reconsideration of Value Guidance to Combat Appraisal Bias

The U.S. Department of Housing and Urban Development (HUD), through the Federal Housing Administration (FHA), recently issued Mortgagee Letter 2024-07 addressing reconsideration of value (ROV) policies in connection with appraisals for FHA insured mortgage loans under the Title II forward mortgage loan and reverse mortgage loan programs. The amended Mortgagee Letter may be implemented immediately but must be implemented for FHA case numbers assigned on or after September 2, 2024. With implementation of the Mortgagee Letter, HUD requires lenders to allow borrowers to request a re-assessment of the appraised value of their property if they believe there is an issue (including bias or discrimination) with the initial valuation. The Mortgagee Letter follows up on action plan items set forth in the Property Appraisal and Valuation Equity action plan jointly issued by HUD and other federal agencies in March 2022.

As outlined by HUD, the new policy includes:

- “A requirement that underwriters be trained to identify and remedy appraisal deficiencies, including racial and ethnic bias;

- Requirements for lenders when receiving, processing, and communicating the status of the reconsideration of value requests initiated by a borrower;

- Standards for lender quality control of appraisal reviews and reconsiderations of value; and

- Standards for appraisers to respond to requests from lenders for a reconsideration of value review.”

- Adding to what constitutes a material deficiency in an appraisal deficiencies “that indicate a potential violation of fair housing laws or professional standards related to nondiscrimination.” The policy also specifies that such deficiencies include “statements related to characteristics of a protected class unless fair housing laws permit consideration of the characteristic, such as age-restricted housing or housing with certain accessibility features.”

- Authorization for an underwriter to obtain a second appraisal without communicating with the appraiser conducting the initial appraisal when “the underwriter considers the Appraiser unable to resolve material deficiencies due to the nature of the deficiency.”

With regard to a borrower-initiated ROV, the Mortgagee Letter provides that a lender “must establish an appeal process that includes steps for the Borrower to receive a copy of the appraisal report and request an ROV when the Borrower believes the appraisal report is inaccurate or deficient.” The Equal Credit Opportunity Act and Regulation B currently require a mortgage lender to provide the applicant with a copy of any appraisal or other written valuations for loans to be secured by first liens on a dwelling, and the Truth in Lending Act and Regulation Z require mortgage lenders to provide an applicant with a copy of any written appraisal performed in connection with a higher-priced mortgage loan.

On the same day that HUD issued the Mortgagee Letter, FHFA announced that, with its assistance, Fannie Mae and Freddie Mac (the Enterprises) published new ROV policies, that are meant to provide clear requirements for lenders to disclose and outline the ROV process for consumers, standardize communication to appraisers, and establish ROV response expectations. “Consistent standards for lenders and appraisers, coupled with a well-understood process for consumers to challenge appraisal findings, will help ensure that consumers are treated fairly,” said FHFA Director Sandra L. Thompson. The guidance may be implemented immediately and must be implemented for loan with applications dated on or after August 29, 2024.

Consistent with the standards outlined in the amended Mortgagee Letter, Fannie Mae published an update to its Selling Guide, and Freddie Mac published a bulletin on selling standards to address new ROV policies.

Fannie Mae’s guide outlines steps for borrowers, and provides that a borrower initiated ROV request must include: the borrower’s name, property address, effective date of the appraisal, appraiser name, date of the ROV request, and a description of unsupported, inaccurate, or deficient areas in the appraisal report. The borrower’s request should also include additional data, information, and comparable properties (not to exceed five), the related data sources (for example, the MLS listing number), and an explanation of why the new data supports the ROV. The Fannie Mae guide also outlines steps for lenders, in addition to the requirement for lenders to implement written policies for accepting and processing a borrower initiated ROV request. A lender must conduct its own appraisal review and designate an appraiser expert to review the ROV request. To complete the ROV process, a lender must validate the request from the borrower, ensure all necessary information has been collected from the borrower, align its procedures with the Appraiser Independence Requirements, send standardized communications to the appraiser that contain all relevant information about the property and the reason for the ROV, and ensure all documentation and communication related to the appraisal and ROV are retained in the loan file. Lenders are instructed to contact the local appraiser licensing agency if there is evidence of any unacceptable appraiser practice, and contact the proper local and federal agencies if there is suspected overt discrimination.

Freddie Mac’s bulletin includes much of the same guidance, and similarly requires lenders to implement procedures that include steps for borrowers to request a ROV and steps for lender review and resolution. As outlined in the Fannie Mae guidance, lenders are instructed by Freddie Mac to disclose the ROV process to borrowers with instructions for initiating a request, and use standardized communications with appraisers, including instructions for the appraiser to deliver a revised appraisal after a ROV request. Further, as is the case with the Fannie Mae guidance, lenders are instructed to contact the local appraiser licensing agency if there is evidence of any unacceptable appraiser practice, and contact the proper local and federal agencies if there is suspected overt discrimination.

Richard J. Andreano, Jr. & Loran Kilson

CFPB Issues New Report on Price Complexity and Highlights Implications for Junk Fees Initiative

As part of its junk fees initiative, the CFPB released a new report, “Price Complexity in Laboratory Markets.” In its press release about the report, the CFPB states that because it “suggests consumers tend to pay more for products that have more complex pricing structures,” the report “has implications for understanding how junk fees impede fair and competitive pricing in markets like auto loans or mortgages, where consumers have to evaluate extended warranties, add-ons, closing costs, and a wide variety of other fees instead of an all-inclusive price.” According to the CFPB, its findings “contribute to a growing consensus of research and real-world observations showing that junk fees increase overall prices beyond what a fair and competitive market would allow.”

The report is based on experiments with multiple rounds of buyers and sellers interacting in simple markets. In the study, participants acted as buyers and sellers in a series of transactions. In some cases, the products for sale had a single all-in price, while in other cases the prices were split into 8 or 16 sub-prices. The CFPB found that buyers tended to fare worse in the scenarios with more complex pricing. It also found that as average selling prices rose, buyers had more difficulty comparing prices across sellers, and the overall amount paid by buyers rose.

The CFPB’s specific key findings were:

- More complex pricing led sellers to ask, on average, for higher total prices, with sellers’ total asking prices 60 percent higher in markets with 16 sub-prices than in markets with one price.

- More complex pricing led buyers to make more “mistakes,” on average. A “mistake” occurred when a buyer bought the product with the higher total price. Buyers were 15 times more likely to select a higher-priced option in markets with 16 sub-prices than in those with one price.

- More complex pricing led to higher transaction prices, on average. The “transaction price” is the total price of a product bought by a buyer. Transaction prices were 70 percent higher in markets with 16 sub-prices than in those with one price, on average.

- In markets with multiple sub-prices, sellers can compete for sales by increasing their price complexity to cause buyers to make mistakes.

- Increasing market competition generally improved, but did not eliminate, the negative effects of complexity.

In its press release about the report, the CFPB notes that “consumers face complex pricing when shopping for financial products and services” and identifies credit cards, checking and savings accounts, mortgages, and auto loans as products with “complex terms and pricing.” Conspicuously absent from the report, however, is any assessment of the impact of the disclosures required under federal laws and regulations on shopping.

John L. Culhane, Jr. & Kristen E. Larson

Final Guidance on Workplace Harassment Published by EEOC

On April 29, 2024, the U.S. Equal Employment Opportunity Commission (EEOC) issued final guidance on workplace harassment subject to federal employment discrimination laws. Aptly titled, “Enforcement Guidance on Harassment in the Workplace” (915.064), this guidance addresses how harassment based on race, color, religion, sex, national origin, age, disability, or genetic information is defined under EEOC-enforced statutes and provides the analysis for determining whether employer liability is established. The Commission’s press release announcing the publication of this final guidance can be found at this link.

The EEOC initially published proposed guidance on October 2, 2023 and invited the public to comment. Our blog post covering this development can be found at this link. The Commission received approximately 38,000 comments during the course of the comment period, which closed on November 1, 2023.

Recognizing significant changes in the legal, technological, and cultural landscape since the Commission last issued guidance on workplace harassment, the new guidance “updates, consolidates, and replaces the agency’s five guidance documents issued between 1987 and 1999, and serves as a single, unified agency resource on EEOC-enforced workplace harassment law.”

A key issue addressed by the final guidance relates to proliferation of technology in the private lives of the workforce and its potential impact on the workplace. For example, the guidance states that, while employers “generally are not responsible for conduct that occurs in a non-work-related context,” employers “may be liable when the conduct has consequences in the workplace and therefore contributes to a hostile work environment.” Even if it does not occur in a work-related context, “conduct that can affect the terms and conditions of employment” includes “electronic communications using private phones, computers, or social media accounts, if it impacts the workplace.”

The final guidance also examines sexual orientation and gender identity. The guidance unequivocally considers sex-based harassment to include “harassment based on sexual orientation or gender identity, including how that identity is expressed” and gives examples of harassing conduct – e.g., the use of epithets regarding sexual orientation or gender identity; disclosure of an individual’s sexual orientation or gender identity without permission; repeated and intentional use of a name or pronoun inconsistent with the individual’s known gender identity; or the denial of access to a bathroom or other sex-segregated facility consistent with the individual’s gender identity.

The guidance offers detailed definitions and descriptions of key terms and concepts, and also provides dozens of examples and hypothetical fact patterns to assist the reader in navigating a variety of nuanced issues that may exist in the work environment. In addition, the final guidance also addresses systemic harassment and provides links to EEOC harassment-related resources. The Commission has released a concise summary of key provisions of the enforcement guidance, intending to provide a broad overview of the document and issues related to workplace harassment.

Notably, EEOC Commissioner Andrea R. Lucas voted to disapprove the final guidance, for reasons including “the guidance’s assault on women’s sex-based privacy and safety rights at work, as well as on speech and belief rights.” Commissioner Lucas’ statement addressing her vote can be read here.

Ballard Spahr’s Labor & Employment Group regularly assists employers with policies, trainings, and investigations to prevent and address workplace harassment claims.

Shannon D. Farmer & Monica Nugent

CFPB Director Rohit Chopra has released a statement about the proposal issued by the Federal Deposit Insurance Corporation, Office of the Comptroller of the Currency, and Federal Housing Finance Agency to address incentive-based compensation arrangements. The rulemaking is required by Section 956 of the Dodd-Frank Act, which directed the FDIC, OCC, FHA, as well as the Federal Reserve Board, National Credit Union Administration, and U.S. Securities and Exchange Commission, to jointly prescribe regulations with respect to incentive-based compensation practices at certain financial institutions that have $1 billion or more in assets. The proposal re-proposes regulatory text that was previously proposed in June 2016, and seeks public comment on certain alternatives and questions.

In his statement about the proposal, Director Chopra takes aim at the other agencies for the pace of the rulemaking, calling it “highly delayed” and commenting that “[w]hen Congress enacts legislation ordering a regulatory agency to issue rules, this is not simply a suggestion” and that “[t]he rules were supposed to be completed thirteen years ago.” We find Director Chopra’s comments quite ironic, given that the CFPB was directed by Dodd-Frank to issue a small business lending regulation implementing Section 1071 of Dodd-Frank and the CFPB did not finalize that regulation until 2023. In fact, the CFPB did not move forward on the Section 1071 rulemaking until it was required to do so pursuant to court-imposed deadlines.

In his statement, Director Chopra indicates that he “want[s] to highlight a few aspects of the proposal, along with some considerations that would strengthen the rule for the largest financial firms, many of whom were the beneficiaries of emergency actions and public bailouts.” Director Chopra highlights the following:

- The proposal requires the deferral of a portion of an executive’s or employee’s bonus package. Director Chopra suggests that consideration be given to “whether a larger portion of these bonuses should be delayed and whether it should pay out over a longer period of time.”

- The proposal requires firms to consider lowering or forfeiting deferred compensation in a range of negative scenarios, such as big losses or misconduct and to consider clawing back compensation that was already paid out within seven years if negative scenarios later played out. Director Chopra suggests that instead of having firms simply “consider” these actions, consideration be given to making the recovery or lowering of bonuses mandatory.

- The proposal prohibits firms from buying hedges for employees, which would render many of the rule’s provisions useless. Director Chopra suggests that consideration be given to prohibiting highly paid employees from acquiring hedges or other financial instruments to blunt the effect of the rule.

- The proposal prohibits incentive compensation arrangements based solely on revenue or volume metrics. Director Chopra suggests that consideration be given to expanding that prohibition to cover all compensation arrangements that are based on revenue or volume targets without regard to quality of performance or risk management considerations.

We find it disappointing that, in suggesting that that agencies should consider imposing even stronger restrictions than those that have been proposed, Director Chopra makes no mention of the need for the agencies to also consider the rule’s impact on the ability of insured financial institutions to attract highly qualified employees and to not make the rule so restrictive as to impede that ability. The proposal, including the decision to move forward without the Federal Reserve Board and SEC, has been criticized by the banking industry.

Following their announcement last July regarding their plans to coordinate on a range of consumer financial protection issues , the CFPB Director and his European counterpart, the Commissioner for Justice and Consumer Protection of the European Commission, have released a joint statement highlighting some areas those coordinated efforts have identified for ongoing monitoring and particular focus. Reiterating their goals of “ensur[ing] that consumers across the Atlantic have their financial data and privacy respected, not surveilled and misused,” keeping consumer financial markets competitive, avoiding fraud, and providing consumers with tools to navigate emerging systems, the joint statement identified three areas where they have had “staff-level sessions” to-date:

- Buy Now, Pay Later (BNPL) & Over-Indebtedness – The European Commission highlighted its most recent study on European consumers’ over-indebtedness and the expected significant increase in over-indebtedness over the next 10 years while also reporting on the expected growth of BNPL products over the coming years. The CFPB shared an overview of the growth of BNPL in the U.S. as well as aggregate borrower demographic data and the applicability of existing statutes;

- Digital Payment Access – Both organizations addressed the increase in utilization of digital payments and the accompanying risk of fraud, with the CFPB focused on the increasing important role of Big Tech firms, such as Apple and Google, in the digital payment space; and

- Artificial Intelligence – The European Commission identified recent legislation and regulation designed to address the use of automated decision making and the processing of data in consumer financial services. The CFPB identified existing regulations with applicability to the use of AI in consumer financial services. Both organizations emphasized the importance of bolstering their internal technological expertise.

The CFPB and European Commission have agreed to continue their efforts to coordinate their responses to emerging technologies by convening an annual principal-level meeting and bi-annual staff level meetings on these issues as well as “any other shared priorities that emerge.”

Ninth Circuit: Arbitration Clause Prevails in “True Lender” Challenge Against OppFi

In a recent unpublished memorandum opinion in a putative class action, Carpenter et al. v. Opportunity Financial, LLC, the U.S. Court of Appeals for the Ninth Circuit upheld an arbitration clause in an agreement governing loans serviced by fintech Opportunity Financial, LLC (OppFi). After a de novo review of a California U.S. District Court decision denying OppFi’s motion to compel arbitration, the Ninth Circuit vacated the denial of OppFi’s motion and directed the district court to refer the matter to arbitration.

The complaint in Carpenter, like three other putative class actions brought in different states by the same plaintiff’s counsel against OppFi, raised claims that OppFi, not its out-of-state, state bank partner, was the “true lender” on the subject loans, and the interest rates therefore should not be higher than those permitted under the laws of the plaintiffs’ states. In Carpenter and these other putative class actions, OppFi’s marketing and servicing arrangements on behalf of the state banks that made the loans were characterized in the complaint as a “rent-a-bank scheme.” The complaint also raised Racketeer Influenced and Corrupt Organizations Act (RICO) claims and other claims against OppFi. In each of the other three actions, the federal district courts compelled individual arbitration and dismissed or stayed the action, based on the arbitration clause: see our earlier blogs here and here. However, in Carpenter, the district court denied OppFi’s motion to compel arbitration, finding the arbitration clause to be “procedurally unconscionable due to legibility and technological issues, and substantively unconscionable because it impermissibly waives Plaintiff’s substantive rights under the California Financial Code.”

In order for an arbitration clause to be deemed unconscionable under California law, there must be a showing of both procedural and substantive unconscionability. The Ninth Circuit held that the plaintiffs in Carpenter did not show that the arbitration clause was substantively unconscionable:

- The district court held that the arbitration clause was substantively unconscionable because it required the arbitrator to apply Utah law to the loan agreement pursuant to the agreement’s choice of law provision, which, according to the district court, would allegedly “eliminate the substantive basis for [Carpenter’s] claims.” The Ninth Circuit found the district court erred in making this determination because application of the loan agreement’s choice of law provision “must be decided in the first instance by the arbitrator.” The Ninth Circuit distinguished its holding from that in Bridge Fund Cap. Corp. v. Fastbucks Franchise Corp., 622 F.3d 996, 998 (9th Cir. 2010), in which the court determined district courts may conduct a choice of law analysis to invalidate an arbitration clause, pointing out that in Bridge Fund the court did not speculate as to which law the arbitrator might apply but instead just determined which state law applied to the unconscionability question.

- The plaintiffs also argued that the arbitration clause was substantively unconscionable because the arbitrator “must enforce” the loan agreement’s choice of law provision even if doing so would render the loan illegal under California law. According to the Ninth Circuit, this “claim is premature” because “[a]t this interlocutory stage it is not established what law the arbitrators will apply.” The Ninth Circuit noted that “even if California law applies, arbitrators are not required to enforce invalid contracts.”

The California Department of Financial Protection and Innovation (DFPI) case against OppFi is scheduled for trial in March 2025. As we previously blogged, in late October 2023, the Superior Court denied DFPI’s motion for preliminary injunction that sought to force OppFi to stop facilitating loans to California borrowers from its partner FinWise Bank at interest rates above the interest rate cap (generally 36% plus the Federal Funds Rate) imposed by the California Financing Law. The Court explained that valid-when-made concepts under California’s usury law and Constitution, and “obstacle preemption,” served as bases for its denial of the motion.

On June 6, 2024, from 1:00 p.m. to 2:30 p.m. ET, we will be holding a webinar “Interest Rate Exportation Under Attack,” in which we will be covering DIDMCA Section 525 opt-outs, “true lender” and anti-evasion laws, attacks on “valid when made,” and more. Click here to register.

Mindy Harris, Kristen E. Larson, Mark J. Levin & Alan S. Kaplinsky

Last week, we blogged about arguments by Colorado and the FDIC in their briefs opposing a motion for preliminary injunction that would enjoin application of Colorado’s opt-out statute with respect to loans by FDIC-insured state banks located outside of Colorado. We promised to blog again this week with a more detailed discussion of why their arguments are off base. Today, we tackle the central issue of the case: where a loan “is made” for purposes of Section 525.

Everyone seems to agree that the answer lies in discerning Congress’ intent in enacting Section 525. Colorado and the FDIC lament the fact that Congress did not explicitly define the meaning of “made in” for application to Section 525, and offer a tortured and misguided analysis of why they believe Congress intended to allow states to opt-out with respect to loans by out-of-state banks, regardless of where key lending functions are performed. We believe Congress’ purpose is clear, notwithstanding the lack of explicit definition of where a loan is made, when Section 525 is considered in appropriate context and basic principles of statutory construction are applied. In this light, it is unmistakable that the approach advocated by Colorado and the FDIC is plainly wrong. Congress did not intend for a state’s opt-out to apply to loans by banks that are not physically present in the state.

Colorado and the FDIC support their view of Congress’ intent with heavy reliance on case law articulating Constitutional principles as to whether Colorado would be prohibited from regulating loans by out-of-state lenders. Under their approach, if a state has Constitutional authority to regulate a loan, this must mean that the loan is made in that state. Colorado goes so far as to proclaim (falsely) that one of these cases, Quik Payday Inc. v. Stork, “hold[s] that where a borrower is in one state and the lender is in another, the loan is made in the state of the borrower’s location.” The FDIC also relies on Quik Payday and other cases articulating dormant Commerce Clause principles to suggest that courts have held that a loan is made in the state where the borrower is located. However, none of the cases cited actually holds that a loan or other transaction is “made in” one state or another when the parties are located in different states. At most, the line of cases they rely on establishes that the dormant Commerce Clause of the U.S. Constitution would not prohibit either the lender’s state or borrower’s state from regulating an interstate loan since both have significant interests in the transaction. The basis for the defendants’ and FDIC’s argument, apparently, is that Congress also intended to conflate Constitutional authority to regulate with where a loan is made, rather than to establish a location-based test focused on where lending functions occur.

We doubt this was Congress’ intention and believe it is more likely that Congress was aligned with the drafters of the 1974 Model Uniform Consumer Credit Code (Model U3C) in this respect. The Model U3C determines where a loan is made based exclusively on the lender’s location at the time key lending functions occur. However, the extraterritorial provisions of the Model U3C provide that, if the borrower is a resident of the enacting state, the enacting state’s laws apply regardless of where the loan was made “as though the loan were entered into in [the enacting] State.” Contrary to the position advocated by Colorado and the FDIC that a loan is “made in” a state if it is subject to regulation there, the Model U3C (and, incidentally, the version of the U3C in effect in Colorado when DIDMCA was enacted) explicitly distinguishes the location of where a loan is made from where the loan is subject to regulation. If the drafters of the Model U3C understood in 1974 that a loan could be “made in” one state but still subject to regulation in other states as well, there is no reason to believe Congress did not likewise have the same contemplation when it enacted DIDMCA in 1980. Congress did not say interest rate preemption would not apply if an opt-out state had authority to regulate the loan. Section 525 is more specific, providing that preemption would not apply if a loan is “made in” an opt-out state.

Also, the FDIC argues that an out-of-state bank necessarily makes a loan in Colorado whenever the borrower communicates an offer or acceptance of loan terms from the state. The FDIC apparently bases this argument on the fact that all loan contracts are necessarily bilateral, and the location of each party is therefore material to a determination of where the contract is made. But this approach confuses the making of a loan with the making of a loan contract. Under any ordinary understanding of these concepts, a loan contract provides that the lender makes a loan and the borrower receives and repays it. The question, therefore, of where a loan is made depends on where the lender is located when it performs the loan contract, not where the parties create the loan contract.

We don’t believe an explanation of dormant Commerce Clause cases decided after DIDMCA’s enactment or a tortured conflation of contract creation with contract performance is informative as to Congress’ thinking when it limited the scope of loans subject to a state’s opt-out under Section 525. Basic and longstanding rules of statutory interpretation better serve this purpose. In particular, the doctrine of in pari materia (generally, laws of the same subject matter must be construed uniformly) requires a reading of Section 525 that conforms with similar federal interest rate preemption and opt-out legislation, especially in this case where the other legislation was enacted contemporaneously and by the same Congress. When read in this light, we believe it is clear that Congress did not intend for a Section 525 opt-out to apply to loans by banks that are not physically present in the state.

Specifically, in addition to DIDMCA, the 96th Congress (1979-80) enacted interest rate preemption legislation applicable to certain business and agricultural purpose loans (P.L. 96-104 and P.L. 96-161 ), and certain FHA-guaranteed mortgage loans (P. L. 96-153), each of which, like DIDMCA, allowed states to opt-out. The opt-outs under P.L. 96-104 and P.L. 96-161 are substantively identical to Section 525, allowing states to opt-out with respect to loans “made in” the state. Under P.L. 96-153, however, the standard is different, allowing states to opt-out with respect to loans “made or executed in” the state.

It is, therefore, unmistakable that Congress intended to give the opt-out under P.L. 96-153 broader effect than the opt-outs under P.L. 96-104, P.L. 96-161 and Section 525. In our view, the only reasonable way to construe all of this legislation in pari materia is to conclude that the opt-out under P.L. 96-153 applies to loans that are either made by the lender or signed or carried out in the state opting out, while the opt-outs under P.L. 96-104, P.L. 96-161 and Section 525 apply only to loans made by a lender physically present in the state. It is not plausible to argue that the additional words “or executed” should be given no substantive effect.

The opt-out provisions of P.L. 96-153 demonstrate that Congress knew how to expand the scope of loans subject to a state’s opt-out simply by providing that it applies to all loans “made or executed” in the state. Especially considering the contemporaneous enactment of the statutes and their consideration by the same legislative committees, it’s hard to imagine laws that mandate in pari materia application more than DIDMCA and P.L. 96-153. It’s even harder to square their differences with the position advocated by Colorado and the FDIC.

The FDIC’s failure to even mention, let alone account for the distinction between the opt-out under Section 525 and the broader-scope opt-out rights under P.L. 96-153 seriously undermines the agency’s credibility in its amicus brief.

Finally, Colorado and the FDIC are dismissive of the core lending functions test borrowed from FDIC General Counsel Opinion 11 as the appropriate evaluation of where a loan is made. As discussed above, in light of the context of the “made or executed in” opt-out authorization found in similar legislation, Congress’ manifest purpose in enacting Section 525 was to base the determination of where a loan is made on an evaluation of where the out-of-state bank performs the functions involved in making a loan. The factors laid out in GC-11 represent a reasonable and informed framework to implement this purpose that has proven workable in the interstate branching context. It would therefore be a reasonable approach for the court to adopt here. Alternatively, the court could adopt the approach taken by the Model U3C, which would similarly base the determination solely on the lender’s location when certain loan making activities occur. Undoubtedly, the position advocated by the drafters of the Model U3C in 1974 represented the consensus view around the time DIDMCA and similar legislation were enacted.

A hearing on the motion for preliminary injunction is set for May 16.

We will continue to monitor and report developments in this case as they arise.

On June 6, 2024, from 1:00 p.m. to 2:30 p.m. ET, we will be holding a webinar “Interest Rate Exportation Under Attack,” in which we will be covering this topic in great detail. Click here to register.

Ronald K. Vaske, John L. Culhane, Jr., Joseph J. Schuster & Alan S. Kaplinsky

The industry group plaintiffs in NAIB et al. v. Weiser et al., the lawsuit challenging Colorado’s opt-out legislation, have filed their reply to the brief filed by the Colorado Attorney General and Colorado Uniform Consumer Credit Code Administrator in opposition to the plaintiffs’ motion for preliminary injunction. In their reply, the plaintiffs also respond to the amicus brief filed by the FDIC supporting Colorado’s position.

The law at issue is the Depository Institutions Deregulation and Monetary Control Act of 1980 (DIDMCA). Section 521 of DIDMCA applies to insured state banks and tracks Section 85 of the National Bank Act, the statute establishing interest rate authority for national banks, generally allowing banks to charge interest at the rate allowed in the state of their location or a floating rate based on a prevailing Federal Reserve discount rate, whichever is higher. In Marquette, a unanimous decision issued just 15 months prior to DIDMCA’s enactment, the U.S. Supreme Court held that Section 85 allows national banks to “export” the rate authorized in states where they are located on loans made to borrowers in other states. Subsequent case law has construed DIDMCA Section 521 in pari materia with Section 85, thereby granting insured state banks the same rate exportation authority as national banks.

Section 525 of DIDMCA allows states to enact laws opting out of Section 521’s preemptive effect with respect to loans “made in” the enacting state. At issue in the litigation is where a loan is made in the case of loans to Colorado residents by insured state banks located in other states. The industry groups contend that, for purposes of Section 525, loans to Colorado residents by insured state banks located in other states should be deemed “made in” the bank’s home state or the state where key lending functions occur. In its brief, Colorado argues that, for purposes of Section 525, a loan is “made in” the borrower’s state. The FDIC, in its brief, argues that, for purposes of Section 525, a loan is “made in” the state where both the borrower and the lender are located.

In addition to countering Colorado’s argument that the plaintiffs lack standing, their claims are not ripe, and they have no private right of action, the industry groups make the following arguments in their reply brief:

- The reference to where a loan is made in Section 525 necessarily focuses on the party that “makes” the loan, i.e., the loan originator. A bank “makes” a loan where the bank conducts one or more of the core functions associated with loan creation, not where the borrower receives or uses the loan funds. This usage of “make” is not unique to Section 525. Throughout Title 12 of the U.S. Code (which governs banking), banks “make” loans and borrowers “receive” or “obtain” loans. Congress could have chosen to expand Section 525 to “loans made or received in any State” but did not do so. Colorado’s and the FDIC’s interpretations conflate making a loan and making a contract for a loan. While state law could provide that making a contract includes such acts as executing, signing, or delivering the contract, DIDMCA refers only to loans, not loan contracts. The FDIC cannot explain why federal law would impose a shifting standard for “made” that turns on state law about where contracts are generally deemed “made” rather than a uniform federal standard.

- Colorado and the FDIC argue that under principles of statutory construction, there must be a distinction between where a loan is “made” under Section 525 and where a bank is “located” under Section 521 and that this distinction must reflect differences in congressional intent. This argument fails because Section 521 does not only use the word “located” when describing which state’s interest rate limits apply for preemption purposes but also uses the word “made.” (Section 521 states that a bank may “charge on any loan…made” interest pursuant to the limits where the bank is “located.”) As courts and regulators have indicated, determining where a bank is “located” under Section 521 turns on where the bank performed key loan creation functions when it “made” the loan in question. Colorado and the FDIC have not explained why the analysis of where a loan is “made” should ignore the borrower’s location under Section 521 but depend on the borrower’s location for Section 525. Principles of statutory construction create a presumption that the relevant definition of where a loan is “made” by a bank should be the same under both Section 521 and Section 525, which means the borrower’s location has no bearing on where a loan is “made.”

- Colorado and the FDIC rely on Dormant Commerce Clause cases to support their interpretation of where a loan is “made” for purposes of Section 525. Quick Payday and the other cases they cite address only the question whether activity affects a given state sufficiently to allow that state to regulate the conduct within the bounds of the Constitution. While it may generally be true that, for purposes of the constitutional minimum for due process, both states have an interest in regulating the terms and performance of a contract when an offer is made one state and accepted in another, that says nothing about the meaning of “made in” for purposes of Section 525 or the scope of federal preemption for loans by state-chartered banks.

- Federal regulators have consistently followed a function approach in determining where a bank makes a loan in connection with the preemption of state interest rate limits. They have never, until this case, equated where a loan is “made” for preemption purposes with where the borrower resides. In attempting to distinguish itself from its Opinion 11 in which it examined the three non-ministerial loan-making functions to determine where a loan was “made” for purposes of Section 521, the FDIC now claims that it merely used “made” colloquially and did not mean to suggest that a loan is actually or exclusively made in the state where the three functions are performed. Even if credited, the FDIC’s explanation only serves to highlight that the ordinary meaning of where a loan is made refers to the place where the bank performs the functions to create the loan. While the FDIC points to statements in Advisory Opinion 88-45 which provided that “located” in Section 521 must mean something different than “made” in Section 525, the FDIC disavows other language in that opinion which addressed factors to consider when determining where a loan is “made” for purposes of Section 525. The FDIC also ignored that the opinion specifically referenced Marquette in stating that “an analysis of all the facts surrounding a transaction must be used in determining where a loan is ‘made.’” The FDIC now argues that Marquette should have no bearing on how “made in” is interpreted for purposes of Section 525. The FDIC’s inability to articulate statutory definitions that comport with the statutory text, relevant case law, and its own pronouncements underscore the lack of deference that the court should give to the FDIC’ current views.

- Plaintiffs’ interpretation better accords with the principles of federalism animating DIDMCA. While Congress granted states a limited right to opt out of DIDMCA and cap the rates their own state-chartered banks could charge, Section 525 does not authorize states to regulate national banks and allows opt-out states to regulate other states’ banks only to the extent those banks actually perform key loan making functions in the opt-out state. This structure balances the federal government’s interest in regulating national banks with states’ interest in regulating their own chartered banks. Colorado is contending that Section 525 empowers it to override other states’ interest-rate regimes and impose its own regulations on all state banks that extend credit to borrowers who are physically located in Colorado even if, under federal law, the bank is located in and makes the loan in a different state. Congress’s goal in enacting DIDMCA was to ensure that during a time of high inflation and high federal interest rates, state banks would be on par with national banks and could lend in their own states or elsewhere at the greater of the federal discount rate (plus 1%) or their own states’ interest rate caps. Thus, the Section 525 opt-out was intended to restore states’ ability to control the rates at which their own state banks loaned money by removing their ability to lend at the federal rate and was not intended as a tool to allow opting out states to reach into other states to regulate the interest rates charged by those states’ banks.

Ronald K. Vaske, John L. Culhane, Jr., Joseph J. Schuster & Alan S. Kaplinsky

Colorado has become the first state to pass legislation (SB24-205) regulating the use of artificial intelligence (AI) within the United States. This legislation is designed to address the influence and implications, ethically, legally, and socially, of AI technology across various sectors.

Any person doing business in Colorado, including developers or deployers of high-risk AI systems that are intended to interact with consumers. The bill defines a high-risk AI system as any AI system that is a substantial factor in making a consequential decision. Notably it does not include (among others) anti-fraud technology that doesn’t use facial recognition, anti-malware, data storage, databases, video games, and chat features so long as they do not make consequential decisions.

The bill includes a comprehensive framework governing the use of AI within government, education, and business with a focus on promoting ethical standards, transparency, and accountability in AI development and deployment. The bill requires disclosure for the use of AI in decision-making processes, sets out ethical standards to guide AI development, and provides mechanisms of recourse and oversight in cases of AI-related biases or errors. These recourse mechanisms include opportunities for consumers to correct any incorrect personal data processed by a high-risk AI system as well as an opportunity to appeal an adverse decision made by a system with human review (if possible). The disclosure requirements will apply to developers, requiring a publicly available statement that describes methods used to manage risks of algorithmic discrimination.

The bill requires the development of several compliance mechanisms if an entity uses high-risk AI systems. These include impact assessments, risk management policies and programs, and annual review of the high-risk systems. These mechanisms are designed to promote transparency in the development and use of these systems.

The passage of this bill positions Colorado at the forefront of AI regulation in the US, setting a precedent for other states and jurisdictions grappling with similar challenge.

Gregory P. Szewczyk, Madison Etherington & Kelsey Fayer

PA Department of Banking and Securities: Virtual Currency Is “Money”

On April 20, 2024, the Pennsylvania Department of Banking and Securities (DoBS) issued a policy statement (Policy Statement) to “clarify” that the Department’s interpretation of the term “money” in the Pennsylvania Money Transmitter Act (MTA) includes “virtual currency, such as Bitcoin.” The MTA provides in part that “[n]o person shall engage in the business of transmitting money by means of a transmittal instrument for a fee or other consideration with or on behalf of an individual without first having obtained a license from the department.’”

Thus, the Policy Statement means that virtual currency exchangers and related businesses doing business in Pennsylvania must become licensed as money transmitters. The effective date of the Policy Statement is October 15, 2024. Neither the DoBS nor the MTA define “virtual currency.”

The Policy Statement provides in pertinent part:

“Money” is defined in the act as “currency or legal tender or any other product that is generally recognized as a medium of exchange.” See 7 P.S. § 6101 (Emphasis added). Virtual currency is increasingly and widely accepted as a method of payment throughout the United States and can be used to purchase goods and services in thousands of physical locations and online. This statement of policy is intended to clarify to the regulated community that the Department includes virtual currency under its interpretation of “money” under the [MTA] and in Chapter 19 because virtual currency is a product that is generally recognized as a medium of exchange. In practice, this means that the Department expects that all persons engaged in the business of transmitting virtual currency by means of a transmittal instrument for a fee or other consideration will obtain a license from the Department, if they have not yet done so.

The “clarification” offered by the Policy Statement is in fact a reversal by the DoBS. In January 2019, the DoBS had issued guidance (Prior Guidance) declaring that virtual currency, “including Bitcoin,” was not considered “money” under the MTA. Therefore, the Prior Guidance stated that the operator of the typical virtual currency exchange platform, kiosk, ATM or vending machine did not represent a money transmitter subject to Pennsylvania licensure. The Policy Statement does not acknowledge the Prior Guidance.

The Prior Guidance in part explained why many virtual currency exchangers were not subject to licensure in Pennsylvania as money transmitters. We provide this prior language because it now presumably describes, at least in part, who will be subject to licensure as of October 15.

Several of the entities requesting guidance on the applicability of the MTA are web-based virtual currency exchange platforms (Platforms). Typically, these Platforms facilitate the purchase or sale of virtual currencies in exchange for fiat currency or other virtual currencies, and many Platforms permit buyers and sellers of virtual currencies to make offers to buy and/or sell virtual currencies from other users. These Platforms never directly handle fiat currency; any fiat currency paid by or to a user is maintained in a bank account in the Platform’s name at a depository institution.

Under the MTA, these Platforms are not money transmitters. The Platforms, while never directly handling fiat currency, transact virtual currency settlements for the users and facilitate the change in ownership of virtual currencies for the users. There is no transferring money from a user to another user or 3rd party, and the Platform is not engaged in the business of providing payment services or money transfer services.

The Prior Guidance provided a similar analysis regarding virtual currency kiosks, ATMs and vending machines.

The approach of the various states regarding whether virtual currency exchangers represent money transmitters subject to state licensure can represent a confusing and fractured regulatory landscape, sometimes made more difficult by vague and old statutes, and/or lack of administrative guidance. However, the general trend – as exemplified by this latest move by Pennsylvania – is to include virtual currency within the ambit of state money transmission laws.

State money transmitter law violations can become federal violations. As we repeatedly have blogged (for example, see here), it is a federal crime under 18 U.S.C § 1960 to operate as a money transmitter business without a required state money transmitting license. Further, administrators or exchangers of digital currency represent money transmitting businesses which must register with Financial Crimes Enforcement Network (FinCEN) under 31 U.S.C. § 5330 as money services businesses (MSBs), which in turn are governed by the Bank Secrecy Act and related reporting and anti-money laundering compliance obligations. Failing to register with FinCEN as a MSB when required is a separate violation of Section 1960, as exemplified by numerous enforcement actions in recent years (for example, see here).

Peter D. Hardy, John D. Socknat & Marjorie J. Peerce

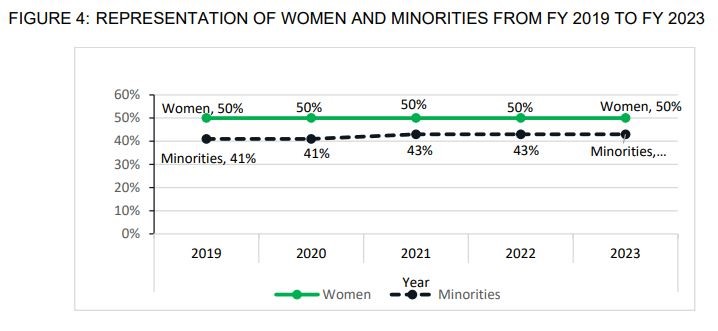

CFPB’s Office of Minority and Women Inclusion Publishes Annual Report to Congress

The CFPB’s Office of Minority and Women Inclusion (OMWI) provided its annual report to Congress covering the agency’s efforts in 2023. Section 342 of the Dodd-Frank, Wall Street Reform, and Consumer Protection Act (Dodd-Frank) mandates that the OMWI agency provide an annual report to Congress regarding the successes achieved, challenges, and other findings.

In 2023, the CFPB engaged in a year-long internal strategic planning effort to further mature diversity, equity, inclusion and accessibility (DEIA). The report highlights the agency’s efforts in carrying out the duties under Section 342 of Dodd-Frank to:

- Increase workforce diversity and build a more inclusive environment within its workplace;

- Ensure fair and inclusive business practices in procurements, contracting, and other business activities; and

- Assess the diversity policies and procedures and practices of entities regulated by the CFPB.

CFPB

The report indicates that in 2023 the CFPB increased minority representation at the executive level to 51 percent (a 5 percent increase from 2022) and women in executive positions equaled 49 percent. Women employees equal 50.4 percent of the agency’s total workforce. Over the past five years, the representation of women employees at the CFPB has remained consistently around 50 percent; however, the representation of minorities has increased from 40 percent to 43 percent.

Contractors & Suppliers

In 2023, minority and women owned businesses earned and received over 40 percent of the agency’s total competitive dollars spent. Both the CFPB’s OMWI and Office of Procurement and Finance has increased minority and women owned business spending from less than 10 percent in 2017 to 41.1 percent in 2023. The Executive Branch has set a goal of 50 percent of Federal procurement dollars to go to small and minority contractors.

Industry

As part of the report, the OMWI collects voluntary self-assessment forms from regulated entities. The report notes that large, non-bank entities were the least likely to submit the self-assessment form. The OMWI analyzes the data provided in the self-assessment forms by industry group, institution size, and responses to questions. Every entity that submitted a self-assessment form engaged in the following activities:

- Included diversity and inclusion considerations in both employment and contracting as an important part of its strategic plan for recruiting and hiring, as well as for promotion and retention;

- Had a diversity and inclusion policy that is approved and supported by senior leadership, including senior management and the board of directors;

- Provided regular DEIA relevant progress reports to the board and senior management;

- Regularly conducted training and provided educational opportunities on equal employment aspects as well as diversity and inclusion;

- Took proactive steps to promote diverse candidates in recruiting, hiring, promotion, and retention efforts, as well as in its selection of board members, senior management, and other senior leadership positions;

- Implemented policies and practices related to workforce diversity and inclusion in a manner that complies with all applicable laws;

- Conducted outreach to educational institutions servicing significant minority and women student populations;

- Utilized both quantitative and qualitative measurements to assess workforce diversity and inclusion efforts;

- Publicized its policy on commitment to diversity and inclusion;

- Prioritized its policy on its commitment to diversity and inclusion;

- Prioritized transparency about its progress toward achieving diversity and inclusion in its workforce and procurement activities, which may include the entity’s current workforce and supplier demographic profiles;

- Publicized its opportunities to promote diversity, which may include current employment and procurement opportunities as well as use of mentorship and developmental programs for employees and contractors;

- Conducted a self-assessment of its diversity policies and practices annually; and

- Monitored and evaluated its performance under its diversity policies and practices on an ongoing basis.

In 2023, the OMWI conducted outreach to the largest non-bank mortgage originators and servicers to encourage self-assessment. During this outreach, the OMWI observed that some entities were unwilling to submit a self-assessment but had robust DEIA programs in place. In 2024, the OMWI intends to focus its outreach efforts on auto financing entities and debt collectors.

The OMWI continues to explore methods to improve the self-submission process.

Ballard’s DEI Counseling team advises clients across industries on the development, implementation, and enhancement of DEI programs. Our attorneys perform assessments, develops strategic plans, advise on existing programs, develop policies and communication materials, conduct training, and facilitate the implementation of DEI programs.

Loran Kilson & Kaley Schafer

Interest Rate Exportation Under Attack

A Ballard Spahr Webinar | June 6, 2024, 1:00 PM – 2:30 PM ET

Speakers: Alan S. Kaplinsky; John L. Culhane, Jr.; Joseph Schuster; Ronald K. Vaske; Mindy Harris; Kristen Larson

Subscribe to Ballard Spahr Mailing Lists

Copyright © 2026 by Ballard Spahr LLP.

www.ballardspahr.com

(No claim to original U.S. government material.)

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, including electronic, mechanical, photocopying, recording, or otherwise, without prior written permission of the author and publisher.

This alert is a periodic publication of Ballard Spahr LLP and is intended to notify recipients of new developments in the law. It should not be construed as legal advice or legal opinion on any specific facts or circumstances. The contents are intended for general informational purposes only, and you are urged to consult your own attorney concerning your situation and specific legal questions you have.