In This Issue:

- Ballard Spahr’s CFS Group and Fintech & Payments Team Nationally Ranked by The Legal 500

- Fannie Mae and Freddie Mac Announce Adverse Market LLPA

- CFPB Issues Promised Seasoned Qualified Mortgage Loan Proposal

- GAO Publishes Report on Effectiveness of Real Estate GTOs Issued by FinCEN

- Fannie Mae and Freddie Mac Announce the End to Purchases of Loans in a COVID-19 Forbearance

- CCPA Regulations Go Into Effect – With a Few Final Changes

- Colorado Administrator Proposes Amendments to Debt Collection Rules

- CFPB Extends Comment Period for RFI on Expanding Credit Access and Further Protecting Consumers From Credit Discrimination

- NY Federal District Court Grants CFPB Petition to Enforce CID Ratified by Director Kraninger

- Financial Institution Regulators Address Financial Inclusion, Expansion of Access to Credit, and Further Consumer Protection From Discrimination

- CFPB Announces Release of HMDA Guides for 2021 Data

- States Issue Work-From-Home Guidance for Mortgage Lenders – Updated August 24, 2020

- Did You Know?

- Looking Ahead

Ballard Spahr’s CFS Group and Fintech & Payments Team Nationally Ranked by The Legal 500

We are pleased to announce that Ballard Spahr’s Consumer Financial Services Group and its Fintech & Payments Team received national rankings from The Legal 500 in the financial services regulation and fintech categories. It was our first application for ranking in the fintech category.

We recently strengthened The Fintech & Payments Team by naming Ron Vaske co-leader, along with James Kim. The team also reorganized to better support Judy Mok and David Medlar‘s transactional practices involving credit cards and other payment solutions.

- Barbara S. Mishkin

Fannie Mae and Freddie Mac Announce Adverse Market LLPA

On August 12, 2020, Fannie Mae and Freddie Mac announced that the cost to originate and to deliver single family limited cash out refinances and cash out refinance mortgage loans would increase by one half of one percent (0.500%), or 50 bps, as a loan level pricing adjustment (LLPA). Fannie Mae Lender Letter (LL-2020-12) states that “[i]n light of market and economic uncertainty resulting in higher risk and costs incurred by Fannie Mae, we are implementing a new [LLPA].” Freddie Mac Bulletin 2020-32 announced its “Market Condition Credit Fee in Price” citing its implementation as a “result of risk management and loss forecasting precipitated by COVID-19 related economic and market uncertainty.” As originally announced, the “Adverse Market Fee,” as referenced by FHFA, was to apply to all whole loans purchased by, or loans delivered into MBS pools with issue dates on or after, September 1, 2020. On August 14, 2020, the Mortgage Bankers Association joined with other housing, financial services, and public interest trade groups in issuing a joint statement on the GSE Adverse Market Fee. On August 25, 2020, FHFA announced that the implementation of the Adverse Market Fee would be delayed until December 1, 2020.

Lenders and Agency Quality Control Firms will understandably focus on the loan origination process and disclosure implications of adding this LLPA to loan pricing. Of particular interest will be how a lender elects to implement the LLPA. For example, potential methods to pass the cost of the LLPA on to the consumer include increasing the interest rate or imposing a fee on the consumer. The method of passing the LLPA on to the consumer will affect the lender’s disclosure obligations on the Loan Estimate and Closing Disclosure, and there may also be other regulatory implications.

For new applications, lenders who plan to pass the LLPA on to the consumer as a charge at consummation should disclose the LLPA as an Origination Charge on the Loan Estimate and Closing Disclosure, pursuant to Comment 5 to 12 CFR 1026.37(f)(1). Because the LLPA is a charge being passed on to the consumer, and not being paid to reduce the interest rate, the LLPA is not disclosed as points, even though it is calculated as a percentage of the loan amount. What the LLPA is labeled on the Loan Estimate and Closing Disclosure can be general, but must clearly and conspicuously describe the service that is disclosed. If, instead, a lender plans to include the cost of the LLPA in the interest rate paid by the consumer, there would be no specific disclosure related to the LLPA. However, if the consumer will pay an amount specifically to reduce the interest rate, that amount would be disclosed as points on the Loan Estimate.

Lenders and QC Firms need to understand the nuances of the various requirements impacted by the new LLPA and the potential of required changes or enhancements to policies and procedures, point of sale or loan origination technology, and document generation systems. For example, various impacts include qualified mortgage loan requirements, APR calculations and tests, and federal and state high cost mortgage loan laws.

CFPB Issues Promised Seasoned Qualified Mortgage Loan Proposal

As promised by the CFPB when it issued two Regulation Z ability to repay rule qualified mortgage (QM) loan proposals in June 2020, the CFPB recently issued a proposal to provide for a new seasoned QM loan. Comments will be due 30 days after the proposal is published in the Federal Register.

The CFPB proposes that the final rule implementing the seasoned QM loan would become effective on the same date as the final rule for the new general QM loan that it proposed in June, and would apply to loans for which the creditor receives the application on or after that date. Loans that meet the seasoned QM loan criteria would qualify for a safe harbor of compliance under the Regulation Z ability to repay rule, regardless of whether or not the loans are higher-priced mortgage loans. Under the ability to repay rule, loans that qualify as a QM loan based on one of the current QM loan categories set forth in the rule are entitled to only a rebuttable presumption of compliance with the rule if they are higher-priced mortgage loans.

The basic proposed requirements for a loan to become a seasoned QM loan are:

- The loan is a fixed rate, first lien loan with a term of no more than 30 years (step rate loans would not be considered fixed rate loans).

- The loan provides for regular periodic payments that are substantially equal and will fully amortize the loan over its term, and the loan does not have an interest-only or negative amortization feature.

- The total points and fees do not exceed the applicable limit for a QM loan.

- The creditor in underwriting the loan takes into account the consumer’s monthly payment for mortgage-related obligations, and considers the consumer’s income or assets and debt, alimony and child support obligations, as well as the consumer’s monthly debt-to-income (DTI) ratio or residual income, and verifies the debt obligations and income.

- The creditor could not sell, assign or otherwise transfer the legal title to the loan before the end of the 36-month seasoning period (calculated from the due date of the first periodic payment), subject to exceptions for transfers required by supervisory action or in connection with a merger or entity acquisition.

- During the 36-month seasoning period the loan may have no more than two delinquencies of 30 or more days, and no delinquency of 60 or more days (if there is a delinquency of 30 or more days when the 36-month point is reached, the seasoning period is essentially extended as it would not end until there is no delinquency).

As noted, a loan that satisfies the requirements at the end of the 36-month seasoning period would become a seasoned QM loan entitled to the safe harbor of compliance. This would be the case for a loan that was a non-QM loan, a rebuttable presumption QM loan under another Regulation Z QM loan category, or even a safe harbor QM loan under another Regulation Z QM loan category. With regard to existing safe harbor QM loans, the CFPB commented that “a Seasoned QM definition would provide additional legal certainty by providing an alternative basis for a conclusive presumption of [ability to repay rule] compliance after the required seasoning period.”

With regard to the requirement that the creditor consider and verify the consumer’s debt, income, etc., compliance with the comparable requirement of any other Regulation Z QM loan category would be deemed to comply with the seasoned QM loan requirement. While the proposal would require the creditor to consider the consumer’s monthly DTI ratio or residual income, it does not set forth any standard for determining what is an appropriate DTI or sufficient residual income. Many lenders and investors avoid non-QM loans because the requirements to consider the consumer’s DTI ratio or residual income and other factors also do not set forth standards to determine acceptability or sufficiency. And in connection with the proposed general QM loan, industry members have expressed concern over the proposed requirement that the creditor consider the consumer’s monthly DTI ratio or residual income because the proposal does not set forth any standard for determining an acceptable DTI or sufficient residual income. Industry members will likely have similar concerns with the proposed seasoned QM loan requirement to consider the consumer’s monthly DTI ratio or residual income.

Under the seasoned QM loan proposal, a temporary payment accommodation provided to a consumer due to financial hardship caused directly or indirectly by a presidentially declared emergency or major disaster under the Robert T. Stafford Disaster Relief and Emergency Assistance Act, or a presidentially declared pandemic-related national emergency under the National Emergencies Act, would not be considered a delinquency, provided that during or at the end of the accommodation the consumer brings the loan current according to the original terms, or there is a qualifying change to the loan. To be a qualifying change: (1) the change would have to end any pre-existing delinquency on the loan when the change takes effect, (2) the amount of interest charged over the full term of the loan may not increase as a result of the change, (3) the servicer may not charge any fee in connection with the change, and (4) the servicer must waive all existing late charges, penalties, stop payment fees, or similar charges promptly upon the consumer’s acceptance of the change. If there is a temporary payment accommodation, the period of the accommodation would not count toward the 36-month seasoning period. The 36-month seasoning period requirement would need to be satisfied by the periods immediately before and after the accommodation period.

To address concerns that a creditor may attempt to take steps to help keep a loan current, (1) if a creditor escrows funds to help cover loan payments, funds taken from the escrow would not be considered in assessing whether a periodic payment has been made or is delinquent, and (2) funds paid on behalf of the consumer by the creditor, servicer, or assignee of the covered transaction (or any other person acting on their behalf) would not be considered in assessing whether a periodic payment has been made or is delinquent. A creditor would be permitted to ignore a partial payment for purposes of assessing delinquency if (1) the creditor chooses not to treat the payment as delinquent for purposes of any of the Regulation X servicing provisions, if applicable, (2) the payment is deficient by $50 or less, and (3) there are no more than three such deficient payments treated as not delinquent during the seasoning period.

The CFPB addressed why it has proposed that the seasoned QM loan apply only to loans for which the application is received on or after the effective date of the rule, and not also to existing loans, stating as follows:

“The Bureau believes that parties to existing loans at the time of the effective date may have significant reliance interests related to the QM status of those loans. In light of these possible reliance interests, the Bureau has opted not to apply the proposal to loans in existence prior to the effective date.” The CFPB also notes that there could be legal issues related to the application of rules governing mortgage origination to loans existing prior to the rule’s effective date.

GAO Publishes Report on Effectiveness of Real Estate GTOs Issued by FinCEN

Law Enforcement Has Been Using GTO Data

First of Two Posts on Evolving Issues Regarding Real Estate and Money Laundering

The U.S. Government Accountability Office (“GAO”) has issued a report on the status and effectiveness of the Geographic Targeting Orders (“GTOs”) issued by the Financial Crimes Enforcement Network (“FinCEN”) since 2016, and on which we repeatedly have blogged. The GAO’s report, entitled “Anti-Money Laundering — FinCEN Should Enhance Procedures for Implementing and Evaluating Geographic Targeting Orders,” (“the Report”) is lengthy. In this post, we will describe the Report at a high level, and will attempt to focus on the portions which shed possible light on two key questions: (1) how is law enforcement using the information culled from filings received by FinCEN as a result of the GTOs; and (2) whether the information obtained from GTO fillings may fuel legislation or regulations that will permanently subject portions of the real estate industry to anti-money laundering (“AML”) reporting requirements under the Bank Secrecy Act (“BSA”).

In our next post, we will turn from regulatory requirements to enforcement actions, and explore some recent high-profile civil forfeiture actions by the Department of Justice — at least some of which may have been fueled by information obtained through GTOs — involving real estate and alleged foreign corruption. Under any scenario, these forfeiture actions confirm the U.S. government’s sustained focus on real estate as a mechanism for money laundering.

The GTOs: The Basics

First, some background. The stated purpose of the GTOs is to try to close loopholes in the current AML regime, and identify bad actors who may be laundering money and concealing their identities through the use of legal entities, such as shell companies, and avoiding the BSA/AML systems of banks by conducting all-cash real estate deals with no loans.

As the Report notes, the BSA includes “persons involved in real estate closings and settlements” in its definition of a “financial institution” subject to the BSA. However, despite issuing in 2003 an advance notice of proposed rulemaking on AML programs for persons involved in real estate closings and settlements (a group which could include attorneys), FinCEN never issued final regulations – except for finalizing a rule in 2012 which required nonbank residential mortgage lenders and originators to establish AML programs and file Suspicious Activity Reports (“SARs”). According to the Report, “[t]his rule subjected the majority of residential real estate transactions to BSA/AML protections and safeguards.” But a major gap remained: residential purchases done without loans. Thus the GTOs.

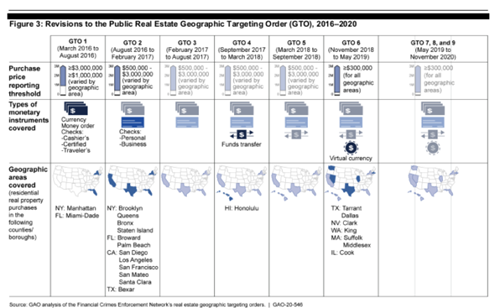

FinCEN has issued a series of GTOs since 2016; each GTO has been effective for a period of six months. On May 8, 2020, FinCEN issued its most recent GTO regarding certain real estate transactions. Specifically, these GTOs require U.S. title insurance companies to identify the natural persons behind legal entities used in purchases of residential real estate performed without a bank loan or similar form of external financing. The current monetary reporting threshold is $300,000. The GTOs now broadly cover purchases involving virtual currency as well as “fiat” currency, wires, personal or business checks, cashier’s checks, certified checks, traveler’s checks, a money order in any form, or a funds transfer. Nine jurisdictions are currently covered by the GTOs.

Purchases made through publicly traded companies are excluded, because their beneficial owners are identifiable through business filings. As the Report notes, one tactic for a bad actor to evade a GTO filing is simply to forego title insurance when making a purchase.

The Report explains that for each GTO renewal, FinCEN assessed the percentage of reported transactions involving a legal entity, purchaser representative, or beneficial owner who was separately the subject of a filed SAR. FinCEN found that the percentage varied across time and geographic area. The GTO filings sometimes helped identify potential suspects of interest for further investigation and led to law enforcement referrals. Thus, the current GTO represents a progression of expanding coverage since the first GTO issued by FinCEN, as reflected by this graphic in the Report regarding changes over time:

Click here to view a larger version

Findings of the Report

The Report, compiled at the request of the U.S. Senate Judiciary Committee, Subcommittee on Crime and Terrorism, summarizes its conclusions as follows:

Unlike prior GTOs, which FinCEN officials said they issued at the request of and with the involvement of law enforcement agencies, FinCEN issued the real estate GTO on its own initiative. Thus, FinCEN had to take the lead in implementing and evaluating the GTO but lacked detailed documented procedures to help direct the GTO’s implementation and evaluation – contributing to oversight, outreach, and evaluation weaknesses. For example, FinCEN did not begin examining its first title insurer for compliance until more than 3 years after issuing the GTO and did not assess whether insurers were filing all required reports. Similarly, while FinCEN initially coordinated with some law enforcement agencies, it did not implement a systematic approach for outreach to all potentially relevant law enforcement agencies until more than 2 years after issuing the GTO. FinCEN also has not yet completed an evaluation of the GTO to determine whether it should address money laundering risks in residential real estate through a regulatory tool more permanent than the GTO, such as a rulemaking. Strengthening its procedures for self-initiated GTOs should help FinCEN more effectively and efficiently implement and manage them as an anti-money laundering tool.

FinCEN responded to the Report in part by noting that its newly-created Global Investigations Division is in the process of reviewing and revising the GTOs’ standard operating procedures.

The Use of GTOs by Law Enforcement

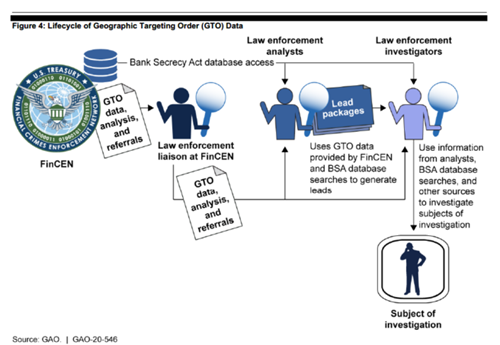

Not surprisingly, law enforcement representatives reported to the GAO that GTO filings provided information which sometimes initiated investigations, or more likely, provided a “secondary source” of information to assist ongoing investigations. More specifically, law enforcement representatives told the GAO that, in addition to serving as investigative leads, information from GTO filings assisted in identifying assets for seizure or forfeiture; using the underlying documents associated with a GTO filing as evidence in support of prosecutions; and “strategic analysis” — that is, the identification of patterns or trends in illegal activity. One example of such strategic analysis was that law enforcement agents were “able to associate GTO reporting with foreign actors, SAR activity, and high-risk AML typologies otherwise not found in the original GTO filings.” Officials also have been tracking which title insurance companies were filing the most GTO reports.

The Report contains the following graphic regarding potential use of GTO data by law enforcement:

Click here to view a larger version

Some law enforcement representatives told the GAO that it was too early to assess fully the usefulness of the GTOs, because the amount of data received has been enormous — all of which takes significant time and resources to analyze — and the true value of information cannot be assessed until the end of investigations, which can take years to complete. Nonetheless, some law enforcement representatives generally supported making the GTO requirements permanent, because the GTOs generated investigative leads and acted as a general deterrent against money laundering.

Future Legislation or Regulation?

The Report observes that the GTOs attempt to address a major problem in AML and money laundering enforcement: the fact that, currently, many states do not require beneficial ownership (“BO”) information when legal entities are formed, coupled with the use of shell companies by bad actors to disguise beneficial owners. This combination can stymie law enforcement, particularly when there are layers of entities. As the Report notes, a national registry regarding the beneficial owners of legal entities has been proposed repeatedly by Congress, and such legislation may yet pass.

The legislation which has been proposed regarding a national registry of beneficial owners share the following general requirements:

- requiring certain corporations and limited liability companies to register at formation or when any changes are made to their ownership structure;

- defining beneficial owners as individuals with greater than 25 percent ownership in the corporation or limited liability company;

- reporting the name or names of beneficial owners in a registry (or database); and

- having a federal agency (such as FinCEN) maintain but limit access to the registry, such as to law enforcement on a “need-to-know” basis.

The Report states that government officials who spoke with the GAO generally supported such legislation in order to close AML enforcement loopholes. Not surprisingly, small business groups opposed such a registry, citing compliance costs. The American Bar Association has expressed concerns over invasion of the attorney-client privilege.

The Report poses the question: if a beneficial ownership registry was passed into law, would the GTO requirements — either in the form of continued GTOs, or final regulation — still be necessary? Again, and perhaps not surprisingly, law enforcement representatives supported the simultaneous existence of a national registry and GTO requirements, because (1) the absence of GTO requirements would make it harder to “connect the dots” and link beneficial owners to their real estate purchases; and (2) a national registry may not apply to foreign entities. Although the Report conceded that a dual regime would impose additional costs, it also stressed that the Financial Action Task Force has concluded that a multi-pronged approach to fighting the misuse of legal entities is more effective.

According to the Report, FinCEN has not yet evaluated the GTOs to determine next steps and whether to impose AML program and reporting requirements on real estate professionals, including real estate agents and attorneys. Real estate industry representatives and “AML experts” who spoke to the GAO provided “mixed views” on whether AML requirements should extend to real estate professionals. One expert cautioned that the real estate industry is large and de-centralized and ill-equipped for such requirements, and that it would be difficult for a federal regulator to effectively conduct examinations across the industry. One industry group told the GAO that real estate agents have limited ability to identify suspicious activity because they are not involved in the financing of purchases. Conversely, another industry group told the GAO that real estate agents and lawyers should be the subject of any AML requirements because they are much more involved with buyers and transactions than title insurers. The outcome here is far from clear and it appears that FinCEN is still assessing and perhaps waiting to see if beneficial ownership registration legislation passes before deciding whether to propose AML regulation regarding the real estate industry.

In our next post, we will switch from discussing regulatory requirements to concrete enforcement actions, by exploring some recent high-profile civil forfeiture actions by the DOJ involving real estate and alleged money laundering and foreign corruption.

If you would like to remain updated on these issues, please click here to subscribe to Money Laundering Watch. Please click here to find out about Ballard Spahr’s Anti-Money Laundering Team. If you would like to read more on money laundering and real estate, please see this detailed article from Ballard Spahr here.

- Peter D. Hardy & Shauna Pierson

Fannie Mae and Freddie Mac Announce the End to Purchases of Loans in a COVID-19 Forbearance

As previously reported, subject to conditions, Fannie Mae and Freddie Mac will purchase loans in a COVID-19 forbearance if the eligible loans have note dates through August 31, 2020. One of the conditions is an additional pricing adjustment of 5 percent if the borrower is a first-time homebuyer and 7 percent for other loans.

In recently issued updates to their respective COVID-19 selling FAQs, Fannie Mae and Freddie Mac advise that there are no plans to extend the note date past August 31, 2020. For eligible loans with note dates on or before August 31, 2020, the loans must be delivered to Fannie Mae by, and the settlement date with Freddie Mac must be on or before, October 31, 2020. Loans with note dates after August 31, 2020, that go into COVID-19 forbearance after closing will not be eligible for sale to Fannie Mae or Freddie Mac.

As previously reported, legislation introduced in Congress would require Fannie Mae and Freddie Mac to purchase, and FHA to insure, mortgage loans involving a COVID-19 forbearance, or a request or inquiry regarding such a forbearance, without additional conditions related to the forbearance, request, or inquiry.

CCPA Regulations Go Into Effect – With a Few Final Changes

On August 14, 2020, the California Office of Administrative Law (“OAL”) approved in part and withdrew in part the Regulations regarding the California Consumer Privacy Act (“CCPA”). While most of the changes are non-substantive, the OAL withdrew certain provisions of the Regulations and resubmitted them to the Attorney General’s Office for further review. Approved sections went into effect immediately.

Among the more notable provisions withdrawn was 999.305(a)(5), which would have required businesses to obtain express consent from consumers before using previously collected information for a materially different purpose. Rather than obtaining express consent, businesses must comply with Section 1798.100(b) of the CCPA, which prohibits businesses from using personal information “collected for additional purposes without providing the consumer with notice consistent with this section.” Because initial notice can generally be accomplished through an online privacy policy, it appears that updates to an online privacy policy may suffice if a business intends to start using previously collected personal information for an additional purpose.

The OAL also made three changes relating to consumers’ opt-out right: (1) withdrawing a provision that required businesses that substantially interacted with consumers offline to provide notice of the right to opt-out via an offline method; (2) withdrawing a provision that required businesses to make the opt-out process to be “easy” and “require minimal steps”; and (3) requiring businesses to entitle their opt-out page as “Do Not Sell My Personal Information” as opposed to “Do Not Sell My Info.” While the latter change is non-substantive, it is a concrete change that many businesses may need to make.

Finally, while much has been made of the OAL’s withdrawal of a provision stating that businesses may deny a request from an authorized agent that does not submit proof that they have been authorized by the consumer (previously Section 999.326(c)), that may be a change without practical effect. Indeed, Section 999.326(a)(1) still allows businesses to require that a consumer provide the authorized agent with signed permission to submit requests to know or delete. And, similarly, Section 999.315(f) allows businesses to deny a request to opt-out submitted by an authorized agent if the agent cannot provide to the business the consumer’s signed permission. Accordingly, it appears that businesses arguably may be able to deny requests if they are unable to verify that an authorized agent has a consumer’s written permission to submit requests on their behalf.

Under California law, the Attorney General’s Office has one year to resubmit withdrawn sections after further review and possible revision. Whether or not the Attorney General’s Office revises and/or resubmits those provisions will likely be influenced by whether the California Privacy Rights Act is passed on the upcoming ballot.

- Gregory P. Szewczyk, Kim Phan & Philip N. Yannella

Colorado Administrator Proposes Amendments to Debt Collection Rules

Colorado’s UCCC Administrator has proposed amendments to the rules implementing the Colorado Fair Debt Collection Practices Act (CFDCPA). The Administrator also announced that a Zoom stakeholder meeting will be held on August 25 to discuss the proposed amendments and to solicit topics for rulemaking.

The proposed amendments include the following:

- The provision regarding the sale of the right to collect accounts would be revised to provide that “[a] licensee who does not own the debt may not sell the right to collect client accounts to another licensee, but only the right for the first licensee to refer the client to the second licensee.”

- The provision regarding collection costs currently states that a licensee cannot “advise, suggest, or request that a client add collection costs to any existing debt unless such costs are specifically authorized by statute.” The amendment would expand the exception to include when collection costs are specifically authorized “by the contract, agreement, note, or other instrument creating the debt and that are not otherwise prohibited by law.”

- A requirement would be added for collection agencies to retain call recordings for two years in an accessible format upon request by the Administrator.

Other proposed amendments would:

- Increase the time period for a collection agency to provide an account statement to a consumer upon receipt of the consumer’s written request from 10 to 14 calendar days

- Increase the amount a collection agency can charge a consumer for an additional account statement requested during any 12-month period from $5 to $10 per statement

- Increase the time period for a collection agency to provide a written statement to a consumer that a debt has been paid or settled in full from 10 business days after the consumer’s request to 14 calendar days

- Increase the time period for a licensee to refund a payment when a consumer denies or disputes an oral payment authorization from 5 business days of receipt of good funds to 7 calendar days

- Increase the time period for a licensee to return a payment to a consumer if it cannot identify the client account on whose behalf the payment was made from 30 calendar days after the end of the month in which the payment was received to 35 calendar days

- Stefanie Jackman & Matthew A. Morr

The CFPB has extended by 60 days the comment period for its Request for Information (RFI) on how best to create a regulatory environment that expands access to credit and ensures that all consumers and communities are protected from discrimination in all aspects of a credit transaction. Originally set to expire on October 2, the comment period will now close on December 1, 2020.

The Bureau issued the RFI last month in lieu of a holding a symposium on ECOA issues planned for this fall. The information sought in the RFI is designed to help the Bureau explore ways to promote access to credit, identify opportunities to prevent credit discrimination, encourage responsible innovation, and address regulatory uncertainty. In particular, the Bureau seeks to explore “cutting-edge issues” at the intersection of fair lending and innovation and develop “viable solutions” to regulatory compliance challenges financial institutions face in complying with ECOA and Regulation B. Specifically, the RFI lists a set of questions as to which the CFPB seeks public comment on whether it should provide additional clarity or guidance.

- Lori J. Sommerfield

NY Federal District Court Grants CFPB Petition to Enforce CID Ratified by Director Kraninger

On August 18, Judge Kenneth M. Karas of the Southern District of New York, granted the CFPB’s petition to enforce a civil investigative demand that it issued to the Law Offices of Crystal Moroney prior to the U.S. Supreme Court’s Seila Law decision and that was subsequently ratified by Director Kraninger.

Judge Karas made his ruling orally from the bench. However, according to reports of the oral argument before Judge Karas, the Moroney law firm had argued that despite the Supreme Court’s severance in Seila Law of the Dodd-Frank Act provision making the CFPB Director removable only “for cause,” the Bureau continued to be unconstitutional because of its funding mechanism. The Moroney law firm contended that the CFPB’s funding through distributions it requests from the Fed rather than through the regular appropriations process violates the U.S. Constitution’s Appropriations Clause in Article I because it divests Congress of its power of the purse by allowing the Bureau to decide how much funding it receives each year.

Judge Karas is reported to have ruled that the CFPB’s funding mechanism did not violate the Appropriations Clause because Congress had established a formula setting a ceiling on how much the Bureau can obtain from the Fed in annual funding. (A similar constitutional argument has been made by All American Check Cashing in its supplemental en banc brief filed with the Fifth Circuit. The Fifth Circuit, on its own motion, vacated the panel’s ruling that the CFPB’s structure was constitutional and granted rehearing en banc.)

On July 2, 2020, following the Seila Law decision, the CFPB filed a Notice of Ratification stating the Director Kraninger had ratified the issuance of the CID to the Moroney law firm. The CID was originally issued in 2017 and reissued in 2019 under Director Kraninger’s leadership. The district court ruled that Director Kraninger could ratify her own prior invalid action. The ruling would appear to imply that Director Kraninger’s ratification was necessary for the CID to now be valid.

In a press release about the ruling, New Civil Liberties Alliance (NCLA), which represents the Moroney law firm, stated that because Director Kraninger had conceded that the CFPB’s structure was unconstitutional before the CID was reissued in 2019, she “knew she was acting unconstitutionally” when the CID was reissued. According to NCLA, by enforcing the CID, the district court “became the first ever to grant ratification where the ratifier knew what she was doing was unconstitutional in the first instance” and that an appeal was under consideration.

In addition to All American Check Cashing in which the en banc Fifth Circuit will be considering the validity of the CFPB’s enforcement action, the Ninth Circuit, on remand from the Supreme Court in Seila Law, will be considering the validity of the CID issued by the CFPB to Seila Law, and the Second Circuit, in RD Legal Funding, will be considering the validity of the CFPB’s enforcement action.

- Alan S. Kaplinsky

Since early June 2020 when cries for racial justice resulted in a period of social unrest in the U.S., federal and state financial institution regulators have taken meaningful, proactive steps to acknowledge financial inequality issues, reach out to traditionally underserved populations to expand access to credit, and further protect consumers from discrimination. While it remains to be seen whether these initiatives will be effective and produce lasting results, they represent a significant, concerted effort by financial services regulators to promote greater financial inclusion and equality. This blog post contains a summary of those efforts.

FFIEC: On June 5, 2020, the members of the FFIEC (FDIC, OCC, Federal Reserve Board (“FRB”), CFPB, NCUA and the State Liaison Committee) issued an unprecedented statement on the importance of financial inclusion. Albeit brief, the statement underscored the federal and state regulators’ commitment to eradicating racism and discrimination in financial services. The regulators also stated they remain “steadfastly dedicated to ensuring that…financial institutions…provide fair access and fair treatment to everyone in America.”

CFPB: On July 10, 2020, the CFPB issued a request for information (“RFI”) on the Equal Credit Opportunity Act (“ECOA”) and Regulation B seeking public comment on how to expand access to credit and ensure that consumers are protected from discrimination in all aspects of credit transactions. The RFI contains a list of 10 topics on which the Bureau seeks public comment on whether it should provide additional clarity or guidance. CFPB Director Kathleen Kraninger concurrently issued a related blog post explaining that the Bureau seeks to play a leading role in the national conversation about racial inequality by taking action concerning fair treatment and equitable access to credit. Toward that goal, the CFPB is “taking steps to help create real and sustainable changes in our financial system so that African Americans and other minorities have equal opportunities to build wealth and close the economic divide.” According to Director Kraninger, issuance of the RFI – with the objective of establishing clear standards to help minorities – is the first step in that effort. The initial RFI was published for a 60-day comment period, which the Bureau just extended for another 60 days to December 1, 2020 to allow sufficient time for all interested stakeholders to comment. A link to our prior blog post about these developments is available here.

OCC: The OCC announced Project REACh on July 10, 2020 to promote greater access to capital and credit for underserved populations through policy and structural issues at the national and local level. REACh, which stands for Roundtable for Economic Access and Change, brings together leaders from the banking industry, national consumer advocacy and civil rights organizations, business, and technology to identify and reduce barriers that prevent full, equal, and fair participation in the nation’s economy. Founding members include the heads of the National Urban League, NAACP, Latino, Asian American, and Native American groups, top executives from JPMorgan Chase Bank, Citibank, and Wells Fargo, as well as leaders from minority-owned banks. The OCC hosted the first roundtable meeting on July 10 to begin identifying the projects the group will tackle, and three broad areas were identified: (i) promoting full and fair economic participation by reducing the number of “credit invisibles” in the U.S. (i.e., consumers without a credit score); (ii) increasing the inventory of affordable and sustainable housing, and (iii) enhancing the future of minority-owned depository institutions.

OCC and HUD: On July 17, 2020 at the Access to Capital Forum, OCC Acting Comptroller Brian Brooks and HUD Secretary Ben Carson and Senator Tim Scott (R-SC) – a member of the Senate Banking Committee and a leader for social justice – unveiled a new initiative to make affordable housing and capital more available to underserved communities through investments and lending related to Opportunity Zones. Lending and investments may receive credit under the OCC’s new CRA rules if such activities occur in Opportunity Zones that overlap with low- and moderate-income (“LMI”) areas and serve LMI populations. During his speech, Acting Comptroller Brooks highlighted important synergies among the OCC’s CRA final rule, Project REACh and the new initiative. Representatives from TD Bank, PNC and other banks also shared success stories of how Opportunity Zones and CRA investments helped promote the vitality of their communities.

FDIC: The FDIC’s efforts to address issues of economic inequality have focused on the role of minority-owned banks (known as Minority Depository Institutions (“MDIs”)) to ensure that they survive and continue to prosper.

- On June 11, 2020, the FDIC issued its annual report to Congress on “Preservation and Promotion of Minority Depository Institutions,” as required by Section 367 of the Dodd-Frank Act. The report notes that as of December 31, 2019, there were 144 FDIC-insured MDIs with combined total assets of nearly $249 billion and 36,676 employees. The report touted the FDIC’s accomplishments during 2019, which included (i) issuance of a research study on demographics, structural change, geography, financial performance, and social impact of MDIs over a 17-year period; (ii) holding three roundtable discussions among MDIs and large bank executives to facilitate greater lending and community development activities in LMI areas; and (iii) establishment of a new MDI Subcommittee of the Advisory Committee on Community Banking.

- On July 23, 2020, the FDIC released a podcast titled “The Role of Minority Banks.” The podcast featured FDIC Chairman Jelena McWilliams and Alden McDonald, President and CEO of Liberty Bank, an African American-owned and managed bank, who discussed the critical role of Minority Depository Institutions (“MDIs”) in the U.S. banking system. Chairman McWilliams explained that the number of MDIs is declining and the FDIC seeks to reverse that trend. Mr. Alden explained how MDIs serve the financial needs of communities of color and contribute to their economic well-being. He also explained that where the U.S. may recover from an economic recession in just a few years, it takes almost 10 years for a minority community to recover. Mr. Alden further explained that if not for MDIs, many individuals of color would have no relationship with a bank whatsoever and would have to resort to other types of lenders that charge high rates and fees.

FRB: Federal Reserve Chairman Jerome Powell has also made several speeches on the U.S. economy in which he has underscored the fact that those who are least able to bear the economic fallout from COVID-19 (minorities and women) are suffering the most and that the Fed is using all of its monetary tools to provide monetary assistance to help them.

FTC: On August 5 and 6, 2020, the FTC hosted a virtual resource fair that was open to the public titled “Working Together to Serve Diverse Communities.” In its invitation, the FTC noted that black, Latino, and other communities of color have been disproportionately affected by the COVID-19 pandemic, which has exacerbated existing economic disparities, and by recent events that require greater attention to justice and equality. The goal of the fair was to provide resources for diverse individuals and communities to access federal services, build stronger relationships, and explore ways that the FTC and other agencies can work together to better serve communities of color. At the fair, nine federal agencies shared information concerning their missions and programs that are available to address these challenges and to strengthen the diverse individuals, families, and organizations that they serve.

- Lori J. Sommerfield

CFPB Announces Release of HMDA Guides for 2021 Data

On August 21, 2020, the CFPB announced the release of the Home Mortgage Disclosure Act (HMDA) Filing Instruction Guide (FIG) for data that must be collected in 2021 and reported in 2022. The CFPB also announced the release of the Supplemental Guide for Quarterly Filers that also applies to 2021 data. HMDA requires the quarterly reporting of data only for financial institutions that reported for the preceding calendar year at least 60,000 covered loans and applications, combined, exclusive of purchased covered loans. In connection with the announcements, the CFPB notes that based on a March 2020 Statement on Supervisory and Enforcement Practices Regarding Quarterly Reporting under the Home Mortgage Disclosure Act, it does not intend to cite in an examination, or initiate an enforcement action, against any institution for failure to report its HMDA data quarterly.

- Richard J. Andreano, Jr.

States Issue Work-From-Home Guidance for Mortgage Lenders – Updated August 24, 2020

In response to the COVID-19 pandemic, state mortgage regulators are daily issuing guidance (1) about whether work from home arrangements are permissible under their existing licensing requirements and/or (2) are granting temporary permission for licenseable activity to occur from unlicensed locations (including employee homes) under specified conditions. Below we identify the states that have issued guidance specifically on this topic. Please note that the scope, duration, conditions and requirements set by the states differ – some even require approval – so please carefully review the state’s guidance set forth at the hyperlink. This is a rapidly changing area so check back regularly for updates and changes.

State Regulators Launch Survey Seeking Input on MLO Licensing Exam

According to the Conference of State Bank Supervisors (CSBS), all state-licensed mortgage loan originators (MLOs) received an e-mail invitation from the State Regulatory Registry, which manages the Nationwide Multistate Licensing System (NMLS) on behalf of state regulators, requesting their participation in a survey that would gather information on various job functions as part of a process to ensure the validity of the nationwide MLO licensing exam.

In accordance with the federal Secure and Fair Enforcement for Mortgage Licensing Act of 2008 (SAFE Act), which requires the NMLS to develop a qualified written test to measure candidates’ knowledge and skills needed for the profession, this survey will inform state regulators of the efficacy of the test. The survey closes on September 25.

Reminder for MLOs to Complete Annual Continuing Education for 2020

The federal SAFE Act requires state-licensed mortgage loan originators (MLOs) to complete a minimum of eight (8) hours of NMLS-approved continuing education (CE) courses annually, in addition to other state-specific requirements, as a condition of license renewal. While the deadline to complete CE requirements in most states is December 31, some states, such as Georgia, have an earlier deadline of October 31.

The NMLS resource chart, which includes state-specific education requirements, deadlines, and FAQs, is available here.

- Aileen Ng

MBA’s Human Resources Virtual Symposium

September 10, 2020

Speakers: Meredith S. Dante & Richard J. Andreano, Jr.

Practising Law Institute Seminar

Practising Law Institute’s 25th Annual Consumer Financial Services Institute

December 7-8, 2020

Speakers: Alan Kaplinsky, Christopher J. Willis

Copyright © 2020 by Ballard Spahr LLP.

www.ballardspahr.com

(No claim to original U.S. government material.)

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, including electronic, mechanical, photocopying, recording, or otherwise, without prior written permission of the author and publisher.

This alert is a periodic publication of Ballard Spahr LLP and is intended to notify recipients of new developments in the law. It should not be construed as legal advice or legal opinion on any specific facts or circumstances. The contents are intended for general informational purposes only, and you are urged to consult your own attorney concerning your situation and specific legal questions you have.